Concerns Rise Over 40% Increase in Closing Costs Impacting Homebuyers' Mortgage Process

- LendingTree may face rising closing costs, projected to increase by 40% to 50% by 2026 for homebuyers.

- The MBA suggests using single credit reports for qualified borrowers, potentially simplifying lending processes for companies like LendingTree.

- Adjustments in credit-reporting practices could lower costs for high-scoring borrowers, affecting LendingTree's competitive landscape.

Rising Closing Costs: A Growing Concern for Homebuyers

In recent discussions within the mortgage industry, a contentious issue emerges surrounding the closing costs associated with credit report fees charged by mortgage lenders. These fees, while seemingly minor compared to overall transaction costs, are on track to see steep increases, potentially rising by 40% to 50% by 2026. The Mortgage Bankers Association (MBA) recently expressed its concerns in a letter to the Federal Housing Finance Authority (FHFA), urging the agency to consider allowing lenders to rely on a single credit report instead of the traditional three-bureau "tri-merge" report for borrowers demonstrating solid creditworthiness, specifically those with scores of 700 or above. This recommendation reflects a pivotal shift in mortgage underwriting practices that may significantly affect both lenders and borrowers.

The MBA’s call for reform coincides with broader changes in the mortgage underwriting landscape. Recently, Fannie Mae, a major player in the market, has removed its minimum credit score requirement for loans processed via its automated systems. Historically, many lenders have adhered to a minimum score threshold of 620. Even though homebuyers in today’s market tend to have stronger financial standings—with average credit scores of 734 for first-time buyers and 775 for repeat buyers—there remains apprehension that adjusting how credit reports are used could complicate the closing process. The proposed change in credit-reporting practices signifies an intersection of regulatory influence and competitive practices, raising multiple considerations about consumer protection, transparency, and agency oversight.

With the FHFA overseeing both Fannie Mae and Freddie Mac, any adjustments to credit-reporting standards or the associated fees can ripple throughout the housing market. Many lenders rely on these government-sponsored enterprises for selling their mortgages, thereby entrenching the influence of Fannie Mae and Freddie Mac in shaping industry practices. If changes recommended by the MBA gain traction, they could simplify processes for lenders, potentially lowering costs for high-scoring borrowers. However, there is skepticism regarding the implications this could have on consumer protections, as critics caution that reducing the redundancy of credit evaluations may expose borrowers to unforeseen risks. The ongoing dialogue between lenders, regulators, and advocacy groups is essential to maintain oversight and protect stakeholders in the evolving market.

In other notable developments, the ongoing discussions highlight the tension between operational efficiency and consumer protection within the mortgage lending industry. As the market faces heightened scrutiny over fees that affect homebuyers' overall costs, stakeholders are compelled to navigate these changes carefully, as they may redefine competitive landscapes and consumer experiences in the future context of home financing. The outcome of this debate will likely have lasting repercussions for how lenders operate and how consumers approach home purchasing, impacting the dynamics of an already complex housing market.

Related Cashu News

Blackstone Mortgage Trust Launches $450 Million Senior Secured Notes for Financial Stability

Blackstone Mortgage Trust (Ticker: UNDEFINED) has initiated a private offering of US$450 million in senior secured notes due in 2031, marking a strategic move to strengthen its capital structure. This…

![AllianceBernstein Partners with Brookfield and Carlyle to Launch ABC [ONE] Retirement Solution.](https://firebasestorage.googleapis.com/v0/b/cashuapplication.appspot.com/o/cashuNewsData%2Fe612a612bbd7a184b952afc6b0cafecacfe232d3%2Fnews_e612a612bbd7a184b952afc6b0cafecacfe232d3.png?alt=media&token=019545694f4417154e316de7809f1ae8)

AllianceBernstein Partners with Brookfield and Carlyle to Launch ABC [ONE] Retirement Solution.

AllianceBernstein Holding L.P. (Ticker: UNDEFINED) collaborates with Brookfield Asset Management and Carlyle to launch an innovative retirement solution, ABC [ONE], aimed at enhancing asset class dive…

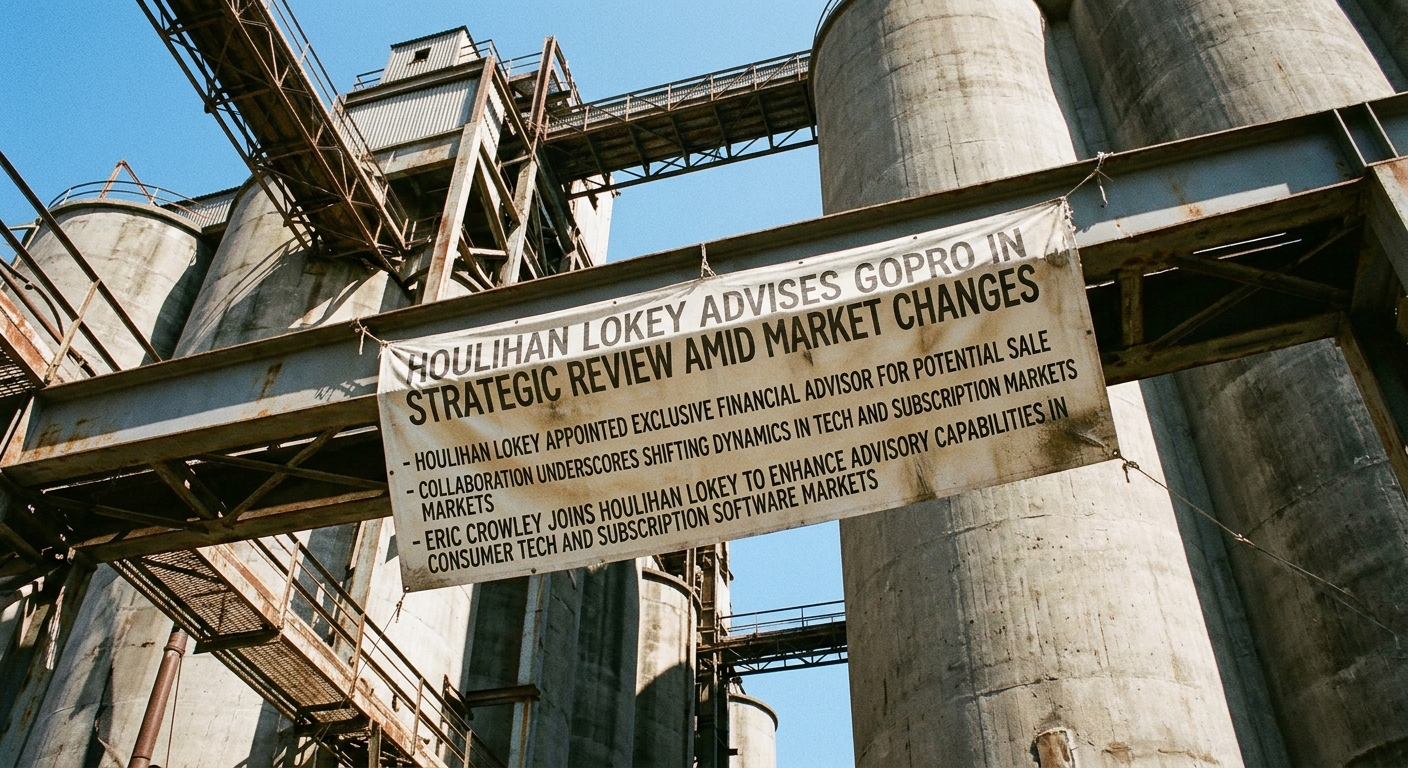

Houlihan Lokey Advises GoPro in Strategic Review Amid Market Changes

Houlihan Lokey (Ticker: HLI) has recently been appointed as the exclusive financial advisor to GoPro, a well-known consumer electronics company. This appointment marks a pivotal moment as GoPro embark…

Federated Hermes Announces Steve Chiavarone as New Chief Investment Officer for Global Equities

Federated Hermes, Inc. (Ticker: UNDEFINED) undergoes a pivotal leadership transition with the appointment of Steve Chiavarone, CFA, as its new Chief Investment Officer for Global Equities, effective S…