Potential Credit‑Card APR Caps Threaten Ally Financial's Consumer‑Lending Model

- Potential APR caps force Ally Financial to reassess underwriting and product strategies.

- Caps would compress Ally's unsecured-lending yields, prompting re-pricing or restriction of risky credit lines.

- Ally is awaiting legislative text and economic analyses while recalibrating products to protect margins and customers.

Ally Financial Faces Policy Crosswinds Over Possible Credit‑Card APR Caps

Potential APR Caps Threaten Ally's Consumer‑Lending Model

Washington's renewed push for statutory caps on credit‑card annual percentage rates (APRs) is forcing banks such as Ally Financial to reassess underwriting and product strategies as policymakers weigh limits that could be as low as 10% or 15%. Ally, which competes in consumer finance and credit cards alongside large issuers, faces a regulatory environment that would compress yields on unsecured lending and prompt re‑pricing or restriction of riskier credit lines. Executives and analysts say such caps would change the economics of card portfolios, alter how banks provision for losses and could shift cost and access outcomes for lower‑income customers.

Banks like Ally are likely to respond by tightening credit availability, narrowing product features or increasing fees to offset reduced interest income, industry participants say. A statutory cap removes a lender’s ability to price loans to borrower risk, which can lead to stricter approval standards, lower credit limits and reduced originations for subprime and near‑prime borrowers. For a lender with mix of deposits, auto finance and consumer credit, the result is a shift in balance‑sheet decisions toward secured lending or fee‑based services where yields are not subject to a single statutory limit.

Regulatory uncertainty also boosts operational and capital planning costs as lenders model scenarios for different cap levels and durations, and prepare for potential consumer remediation and compliance programs. Ally and peers are awaiting concrete legislative text and independent economic analyses that would quantify the trade‑offs between consumer relief from high APRs and the risk of shrinking credit access. In the near term, Ally is likely to engage with industry groups and regulators while recalibrating product offerings to protect margins and preserve relationships with retail and auto finance customers.

Bipartisan Political Momentum

The bipartisan momentum driving the debate ranges from former President Donald Trump’s call for a one‑year 10% cap to Senator Bernie Sanders’s push for a permanent 15% cap, with Senator Josh Hawley and Senator Elizabeth Warren also backing legislative limits. Lawmakers are signaling that they expect concrete proposals and cost estimates before pushing measures through Congress.

Industry Pushback and Broader Economic Concerns

Large banks warn that aggressive caps would curtail lending broadly and ripple through consumer spending that fuels much of the U.S. economy, while issuers such as Capital One publicly note that sharp rate limits could trigger immediate credit‑line cuts and reduced new originations. Policymakers, lenders and consumer advocates now await detailed economic studies to inform next steps.

Related Cashu News

Blackstone Mortgage Trust Launches $450 Million Senior Secured Notes for Financial Stability

Blackstone Mortgage Trust (Ticker: UNDEFINED) has initiated a private offering of US$450 million in senior secured notes due in 2031, marking a strategic move to strengthen its capital structure. This…

![AllianceBernstein Partners with Brookfield and Carlyle to Launch ABC [ONE] Retirement Solution.](https://firebasestorage.googleapis.com/v0/b/cashuapplication.appspot.com/o/cashuNewsData%2Fe612a612bbd7a184b952afc6b0cafecacfe232d3%2Fnews_e612a612bbd7a184b952afc6b0cafecacfe232d3.png?alt=media&token=019545694f4417154e316de7809f1ae8)

AllianceBernstein Partners with Brookfield and Carlyle to Launch ABC [ONE] Retirement Solution.

AllianceBernstein Holding L.P. (Ticker: UNDEFINED) collaborates with Brookfield Asset Management and Carlyle to launch an innovative retirement solution, ABC [ONE], aimed at enhancing asset class dive…

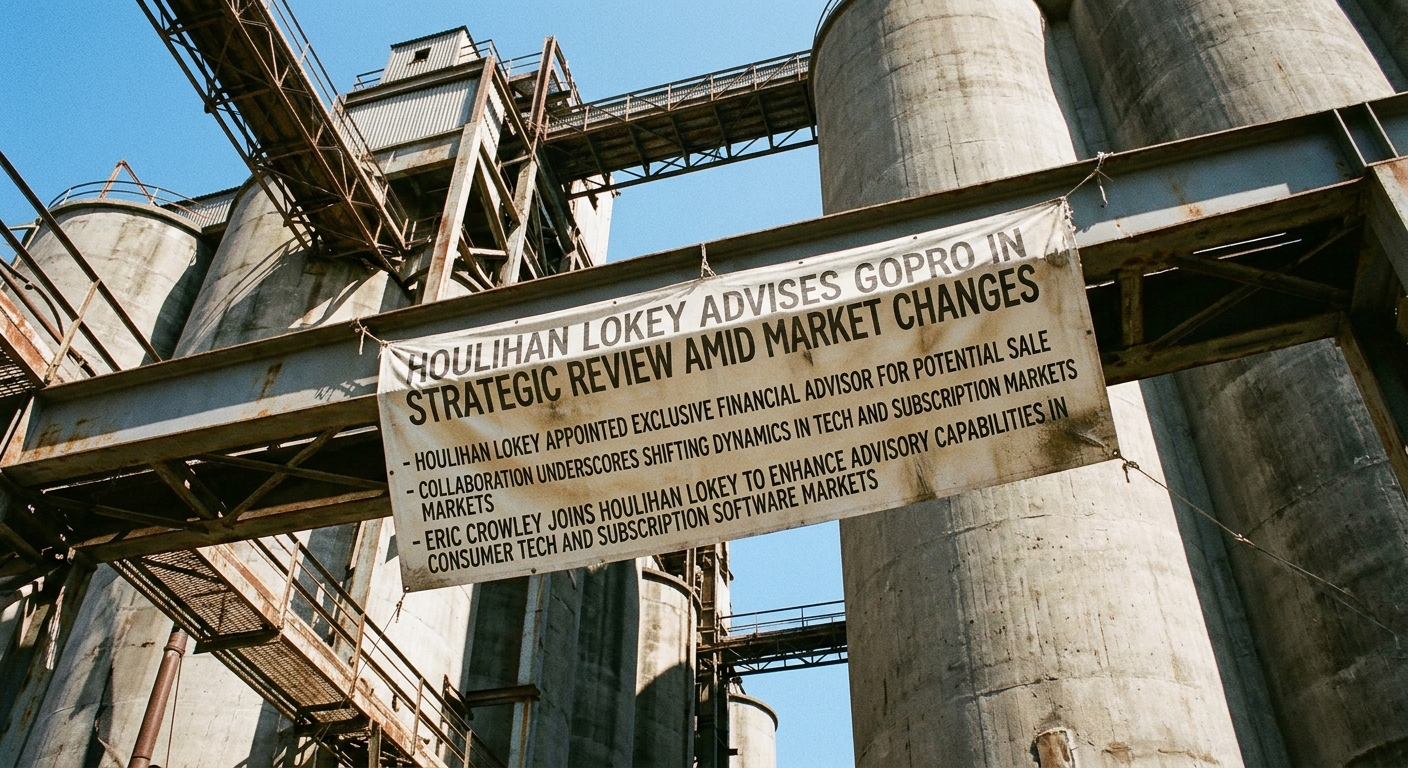

Houlihan Lokey Advises GoPro in Strategic Review Amid Market Changes

Houlihan Lokey (Ticker: HLI) has recently been appointed as the exclusive financial advisor to GoPro, a well-known consumer electronics company. This appointment marks a pivotal moment as GoPro embark…

Federated Hermes Announces Steve Chiavarone as New Chief Investment Officer for Global Equities

Federated Hermes, Inc. (Ticker: UNDEFINED) undergoes a pivotal leadership transition with the appointment of Steve Chiavarone, CFA, as its new Chief Investment Officer for Global Equities, effective S…